Table of contents

- Step 1: Learn About Credit Scores

- Step 2: Review and Monitor Your Credit Report

- 5 Ways To Instantly Boost Your Credit Score

- Step 3: Pay Bills on Time

- Step 4: Lower Your Credit Utilization Ratio

- Step 5: Build a Positive Credit History

- Step 6: Use AI Tools for Credit Improvement

- Step 7: Dispute Credit Report Errors

- Conclusion: Key Steps for Credit Score Improvement

- FAQs

Want to boost your credit score quickly? Here's how:

- Pay bills on time: Payment history is 35% of your score. Automate payments to avoid missing deadlines.

- Lower credit utilization: Keep your usage below 30% of your credit limit. Aim for 7% for the best results.

- Check your credit report: Get free reports weekly at AnnualCreditReport.com. Spot and dispute errors to fix inaccuracies.

- Build credit history: Use secured credit cards or become an authorized user on someone else's account.

- Use AI tools: Platforms like CreditCaptain can monitor your score, detect errors, and suggest ways to improve.

Improving your credit score can save you thousands on loans, mortgages, and insurance. Start now for better financial opportunities.

Step 1: Learn About Credit Scores

What is a Credit Score?

A credit score is a three-digit number, ranging from 300 to 850, that shows how reliable you are as a borrower. Think of it as your financial report card. The higher your score, the more appealing you are to lenders. Generally, a score above 670 is considered good, and anything over 740 is excellent.

Factors Affecting Your Credit Score

Your credit score is based on five main factors:

| Factor | Weight | What It Means |

|---|---|---|

| Payment History | 35% | Tracks whether you pay bills on time. |

| Credit Utilization | 30% | Measures how much of your credit you use. |

| Length of Credit History | 15% | Looks at how long your accounts have been active. |

| Credit Mix | 10% | Considers the types of credit you manage (e.g., loans, credit cards). |

| New Credit | 10% | Accounts for recent credit applications. |

To keep your score in good shape, aim to use less than 30% of your available credit and always pay your bills on time.

Why a Good Credit Score Matters

Having a strong credit score can make a big difference in your financial life. Here's how:

- Lower Interest Rates: With a higher score, you’re more likely to qualify for loans with better interest rates, saving you money.

- Exclusive Financial Products: Premium credit cards and other financial perks are often reserved for those with excellent credit.

Understanding these basics sets you up for success as you work on monitoring and improving your credit. Let’s dive into the next steps!

Step 2: Review and Monitor Your Credit Report

Get Your Free Credit Report

Did you know you can access your credit reports for free every week? Thanks to federal law, you can download your reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com. All you need to do is visit the site, provide your personal details, verify your identity, and download your reports.

Use AI-Powered Credit Monitoring Tools

Technology has changed the way we monitor credit. Tools like CreditCaptain use AI to keep an eye on your credit profile. These systems analyze your credit data and offer tailored suggestions, such as which balances to pay down, how to address inaccuracies, or ways to make the most of your credit utilization.

Here’s what these tools typically track:

| Monitoring Feature | Purpose | Benefit |

|---|---|---|

| Real-time Alerts | Notifies you of credit inquiries/changes | Detects fraud quickly |

| Score Changes | Tracks shifts in your credit score | Understands financial decisions' impact |

| Account Activity | Watches for new accounts or closures | Prevents unauthorized activity |

| Payment History | Monitors bill payment status | Ensures timely payments are recorded |

Using these tools helps you stay ahead of potential issues and make smarter decisions to improve your credit score.

Identify and Correct Errors

Mistakes on credit reports are more common than you might think. In fact, errors were the most reported issue to the Consumer Financial Protection Bureau between 2021 and 2023. As you review your credit report, pay close attention to:

- Account balances, payment histories, and credit limits

- Personal information like your name and address

- Hard inquiries to confirm they were authorized

- Negative marks that should have already been removed

If you find an error, gather proof such as bank statements or receipts. You can file disputes online through the websites of the credit bureaus for a quicker resolution. Filing disputes won’t harm your credit score, and you can challenge as many inaccuracies as needed to ensure your report is accurate.

Once your report is up-to-date and error-free, you’ll be ready to focus on building better payment habits to strengthen your credit score even further.

5 Ways To Instantly Boost Your Credit Score

Step 3: Pay Bills on Time

Your payment history is the single most important factor in your credit score, making up 35% of your FICO score. This means paying your bills on time is absolutely critical if you want to maintain or improve your credit score.

Automate and Monitor Payments

Automating your payments while keeping an eye on your accounts is a smart way to ensure you never miss a due date. Here’s a quick breakdown of how to handle different types of payments:

| Payment Type | Minimum Setup | Recommended Setup | Why It Matters |

|---|---|---|---|

| Credit Cards | Minimum payment | Full balance | Avoids interest charges |

| Utilities | Full amount | Full amount | Prevents service disruptions |

| Loans | Required payment | Extra payment | Pays down the principal faster |

Using tools like Mint or Google Calendar can help you stay on top of your bills. Set up reminders at intervals - like one week before, three days before, and on the due date - to ensure your account has enough funds for automatic payments.

Focus on Debt Payments

If you’re juggling multiple debts, it’s important to prioritize the ones that affect your credit score the most. These include:

- Credit cards

- Personal loans

- Auto loans

- Mortgage payments

To tackle your debt efficiently, you can use either the Debt Avalanche method (pay off high-interest debts first) or the Debt Snowball method (start with smaller balances for quick wins).

Keeping at least one month’s worth of bill payments in your account is a good cushion to avoid overdrafts or missed payments. Late payments can stay on your credit report for up to seven years, but their impact lessens as you build a streak of on-time payments.

Once you’ve mastered timely payments, you’ll be ready to work on improving your credit utilization ratio for even better results.

Step 4: Lower Your Credit Utilization Ratio

Your credit utilization ratio accounts for 30% of your FICO score, making it a key factor after payment history. This ratio reflects how much of your available credit you're currently using.

The 30% Rule Explained

Aim to keep your credit utilization below 30%. For example, if your credit limit is $1,000, try to stay under $300. Research shows that individuals with top credit scores (795 or higher) typically use just 7% of their available credit.

Here’s how different utilization levels can impact your credit score:

| Utilization Range | Effect on Credit Score | Example for $1,000 Credit Limit |

|---|---|---|

| 0-7% | Best | $0-70 balance |

| 8-29% | Good | $80-290 balance |

| 30-49% | Average | $300-490 balance |

| 50%+ | Poor | $500+ balance |

Tips to Lower Credit Utilization

Here are some practical ways to bring down your credit utilization:

- Time Your Payments Strategically: Pay off balances early or make multiple payments within the billing cycle to reduce the amount reported to credit bureaus.

- Spread Out Your Spending: Use multiple cards to distribute your expenses. Both individual card utilization and overall utilization are considered by credit bureaus.

"High credit usage signals overspending and financial strain." - Credit Expert via Experian [2]

Request a Higher Credit Limit

Asking for a credit limit increase is another way to improve your utilization ratio. When making the request, emphasize your on-time payment history and stable income. It’s best to wait at least six months after opening an account before requesting an increase.

"Increasing your credit limit immediately decreases your utilization." - Mike Sullivan, personal finance consultant at Take Charge America [3]

Once you’ve tackled your credit utilization, the next step is to work on building a solid credit history.

sbb-itb-b2789ac

Step 5: Build a Positive Credit History

Creating a strong credit history takes careful planning and consistent, responsible actions. Your credit history is like a financial report card that lenders review to determine how reliable you are with credit.

Become an Authorized User

One way to strengthen your credit profile is by becoming an authorized user on someone else’s credit card. When the primary cardholder has a solid record of on-time payments and low credit card utilization, their positive habits can reflect on your credit file. The timing of any improvement depends on the card issuer’s reporting cycle and the account's status.

"If someone becomes an authorized user on a credit card with a good payment history, they might see improvements in their credit score within 6-12 months." - Credit Expert [1]

To get the most out of this strategy, choose a card with a long history of responsible use and consistent activity.

Use Secured Credit Cards Wisely

Secured credit cards are a great option for those looking to build or rebuild their credit. These cards require a refundable deposit, which acts as your credit limit.

| Feature | Details | Impact on Credit |

|---|---|---|

| Security Deposit | $200-$2,000 typical range | Becomes your credit limit |

| Payment Reporting | Reports to all 3 bureaus | Builds payment history |

| Credit Limit | Matches deposit amount | Affects utilization ratio |

To make the most of a secured card, use it for small, regular purchases and pay off the balance in full each month. Many secured cards transition to unsecured cards after 12-18 months of responsible use.

Diversify Your Credit Types

Your credit mix accounts for 10% of your credit score. Lenders like to see that you can handle different types of credit, such as revolving credit (credit cards) and installment loans (auto or personal loans).

"Having a mix of credit types, such as installment loans and revolving credit, can help improve credit scores. This diversity shows lenders that an individual can manage different types of credit responsibly." [2]

Only take on new credit when it fits your financial goals and you’re confident you can manage it well. Before adding new accounts, make sure your current ones are in good standing.

Once you’ve built a solid credit history, you can explore tools and strategies to take your credit management to the next level.

Step 6: Use AI Tools for Credit Improvement

AI tools have made managing and improving your credit score simpler and more efficient. While traditional methods like paying bills on time and keeping credit utilization low remain important, these tools take credit improvement to the next level.

What AI Credit Tools Offer

AI-powered platforms analyze your credit data to uncover ways to boost your score. They combine automated tracking with tailored suggestions, making credit management easier. Tools like CreditCaptain provide features that simplify the process:

| Feature | Purpose | Advantage |

|---|---|---|

| Real-time Monitoring | Tracks changes in your credit report around the clock | Instant alerts for any updates |

| Error Detection | Uses AI to spot inaccuracies | Helps you address disputes early |

| Automated Disputes | Creates and submits dispute letters | Saves time and ensures precision |

| Score Analysis | Breaks down credit factors | Offers personalized strategies for improvement |

"Users who utilize AI-driven credit management tools see faster and more significant improvements in their credit scores compared to those who do not use such tools." [3]

Some standout features of these platforms include:

- AI-driven credit dispute submissions with no limits

- Tailored score analysis and recommendations

- Goal-focused strategies designed by AI

Why AI Makes a Difference in Credit Optimization

AI tools can analyze your credit profile and suggest specific actions to improve your score faster than traditional methods. They provide continuous tracking, resolve disputes quickly, and offer daily insights into your credit health.

Here’s how AI stands out:

- Pinpoints impactful ways to improve your credit

- Automates repetitive tasks like monitoring

- Delivers actionable, data-based recommendations

- Simplifies the dispute process for better results

While these tools can accelerate your progress, pairing them with good financial habits - like paying bills on time - will lead to lasting improvements. Up next, we’ll dive into effective ways to dispute credit report errors, using both traditional and AI-powered approaches.

Step 7: Dispute Credit Report Errors

Errors on your credit report can hurt your credit score. Did you know that 1 in 5 consumers has mistakes on their credit reports that could lower their scores? [4]

How to File a Dispute

Fixing these errors involves a few key steps and proper documentation:

| Step | Action | Required Documentation |

|---|---|---|

| Gather Evidence | Collect proof of the error | Bank statements, payment records |

| Submit Dispute | File with the credit bureau | Dispute letter, supporting documents |

| Monitor Progress | Track the investigation process | Copies of all correspondence |

Credit bureaus are legally required to resolve disputes within 30 days. Make sure your dispute letter is clear, includes your contact information, and directly requests the correction or removal of the error.

Use AI Tools to Simplify the Process

AI tools like CreditCaptain make disputing errors easier. These tools can create dispute letters, track progress, and ensure compliance with FCRA rules. They help ensure your letters are accurate and increase the chances of resolving your dispute successfully.

Stay on Top of Dispute Outcomes

Keep copies of all communications and check back after 30 days if you haven’t heard back. Once the issue is resolved, confirm that your credit report reflects the correction.

"Credit bureaus are required by law to investigate disputes and correct errors within 30 days, as mandated by the Fair Credit Reporting Act (FCRA)" [1]

If your dispute isn’t resolved, you have additional options:

- File a complaint with the CFPB

- Add a short statement to your credit report explaining the issue

- Consult with consumer protection attorneys for further help

Conclusion: Key Steps for Credit Score Improvement

Improving your credit score takes consistent effort and attention to important factors like payment history (35%) and credit utilization (30%). Building better habits and using available resources wisely can lead to success.

Here are a few practices to stick to:

- Check your credit reports regularly: Ensure accuracy and keep an eye out for any changes.

- Be mindful of credit usage: Aim to keep your credit utilization low.

- Pay on time: Automate bill payments to avoid missed deadlines.

- Expand credit wisely: Gradually build a mix of credit accounts over time.

AI-driven tools, such as CreditCaptain, can make credit management easier. They help by automating monitoring and offering insights you can act on. While these tools are helpful, they work best when combined with disciplined financial habits.

Improving your credit doesn’t happen overnight - it requires patience and commitment. Focus on:

- Building consistent payment habits.

- Using credit carefully and within limits.

- Checking your credit reports frequently.

- Addressing problems quickly when they arise.

"Credit scores are a critical component of financial health, affecting individuals' ability to borrow, achieve financial goals, and build wealth over time" [5].

FAQs

How do you calculate credit utilization ratio?

To find your credit utilization ratio, divide your total credit card balances by your total credit limits, then multiply by 100 to express it as a percentage. This percentage plays an important role in your credit score, so aim to keep it as low as possible [2].

How fast can I add 100 points to my credit score?

You can see noticeable improvements in as little as 45 days by taking specific actions. Paying down your balances, resolving any collections accounts, and catching up on past-due payments are some of the most effective ways to boost your score [2].

What is the most accurate app for your credit score?

Here are some popular credit monitoring apps known for their accuracy and helpful features:

- myFICO: Provides official FICO scores used by lenders.

- Credit Karma: Offers free daily credit estimates and tailored recommendations.

- Aura: Monitors all three credit bureaus and sends quick fraud alerts.

Can AI help me with my credit score?

Yes, AI tools like CreditCaptain can assist with credit management by automating tasks like credit monitoring, spotting errors in your report, and suggesting personalized strategies for improvement. These tools use data-driven insights to make managing and improving your credit simpler [3].

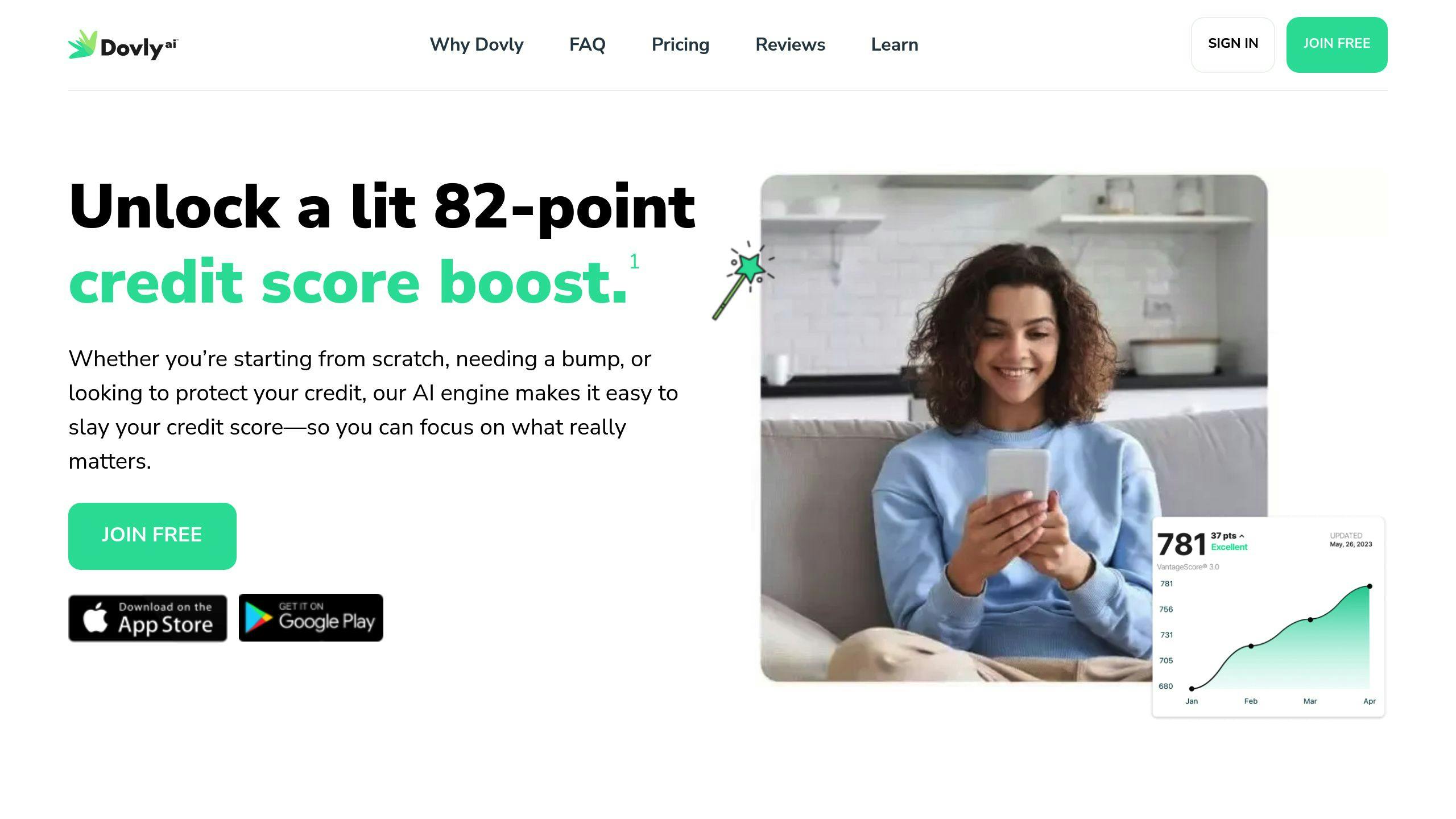

Is Dovly AI real?

Dovly AI is a legitimate service that uses AI to help improve credit. It offers automated credit monitoring and dispute resolution to address inaccuracies on your credit report [3].

These FAQs tackle common questions, but improving your credit requires consistent effort and smart strategies.